Procedural

Requirements

Effective Date: February 23, 2023

Expiration Date: February 23, 2028

|

|

NASA Procedural Requirements |

NPR 9090.1C Effective Date: February 23, 2023 Expiration Date: February 23, 2028 |

| | TOC | Change History | Preface | Chapter1 | Chapter2 | Chapter3 | Chapter4 | AppendixA | AppendixB | AppendixC | AppendixD | AppendixE | AppendixF | AppendixG | ALL | |

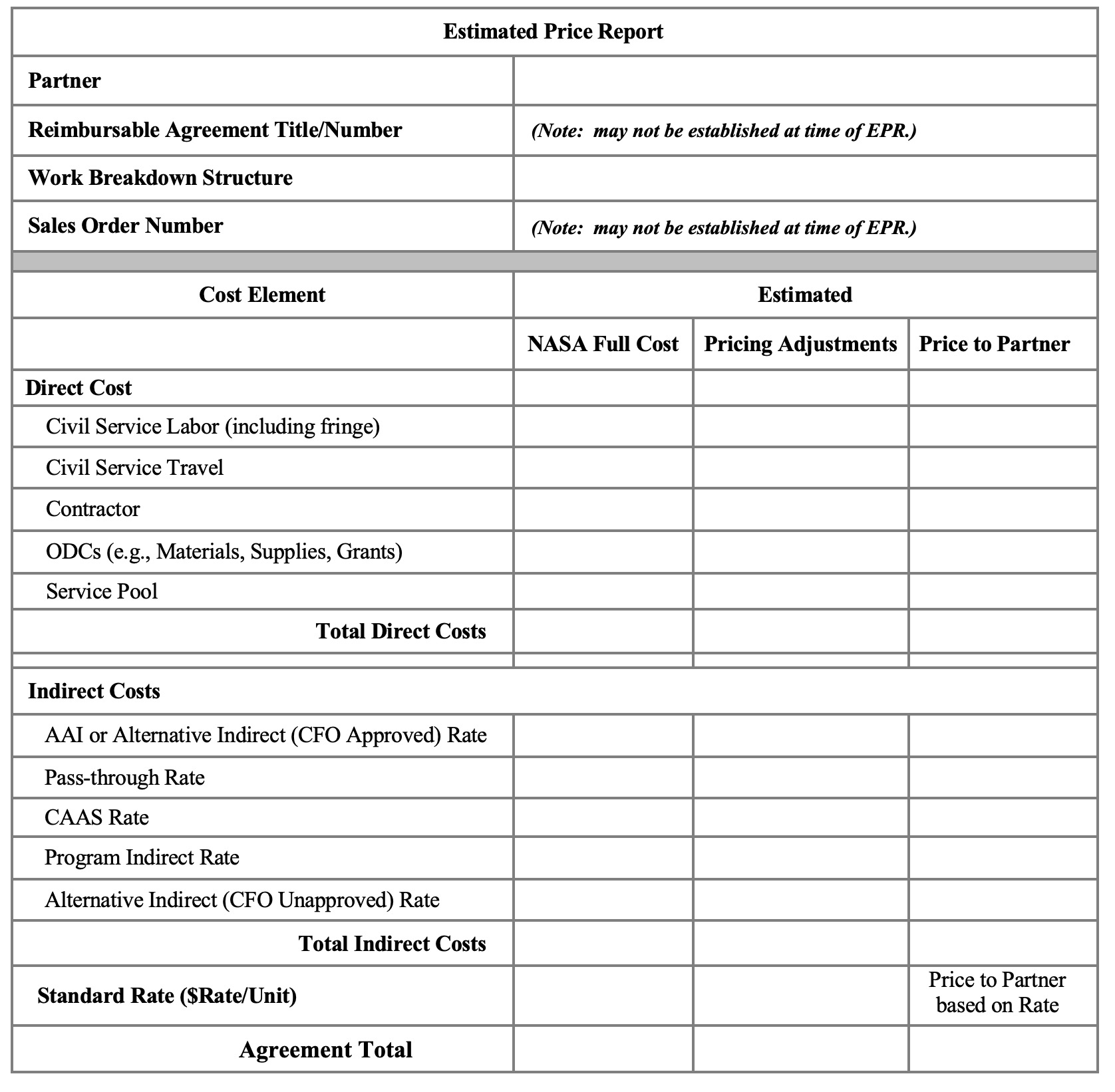

Note: The following template is representative of the minimum requirements for an EPR. Cost elements listed below include those most widely used but may not be applicable to every EPR. Additional cost elements may be included, as needed.

C.1.1 Instructions for Completion of the EPR

a. The EPR shown in this Appendix is a template. A Center may utilize alternative formats at their discretion, but the EPR should include the basic minimum information shown. In any format, the full cost of NASA's effort, the pricing adjustments, and the price to the partner should be apparent.

b. Some information, such as the WBS, sales order number, or other similar accounting classifications used with the accounting system, might not be available when the EPR is initially prepared. However, the information should be included with the final approved EPR as supporting documentation to the agreement.

C.1.1.1 Column 1 - Cost Element. The column identifies the type of costs that make up the full cost of the agreement.

a. Direct Cost Elements:

• Civil Service Labor - Civil service labor costs, to include fringe and paid leave.

• Civil Service Travel - Travel costs of civil servants estimated in performance of the agreement.

• Contractor - Contractor costs in direct support of the agreement.

• ODCs - Materials, supplies, utilities, grants, and other direct costs in support of the agreement. ODCs should be identified by individual line items.

• Service Pool - Service pool costs allocable to the agreement. If more than one service pool is estimated, each one should be identified by individual line items.

b. Indirect Cost Elements:

• AAI or Alternative Indirect (CFO Approved) Rate - AAI costs applicable to the agreement. As identified in section 3.2.3, a Center CFO approved alternative indirect rate can be reflected on this row or a separate designated line but should not be considered a waived cost or a pricing adjustment.

• Pass-Through Rate - Administrative costs associated with agreements that typically identify existing contract(s) that are approved by the Center CFO. Pass-through rate is not considered a pricing adjustment.

• Contract Administration and Audit Services (CAAS) Rate- Procurement services costs subject to audit requirements and exceeds $1 million. CAAS rate is not considered a pricing adjustment.

• Program Indirect Rate - Indirect costs specific to a program that are not part of the AAI rate or other identified costs. Program indirect rate is not considered a pricing adjustment.

C.1.1.2 Column 2 - NASA Full Cost Estimate. This column identifies the estimated full cost for NASA to perform the agreement activity by each cost element in Column 1. The full cost of the agreement should only include work that is specific to the partner for the scope of work identified in the agreement. For standard rate cost estimate, the cost to NASA should be identified by cost element.

C.1.1.3 Column 3 - Pricing Adjustment. This column identifies the waived, excluded, or other authorized pricing adjustments by cost element as outlined in section 4.3, Pricing Adjustments. If the price will reflect a combination of adjustments, the adjustments should be shown separately on the EPR. For standard pricing, pricing adjustments should be identified by cost element.

C1.1.4 Column 4 - Price to Partner. This column identifies the estimated price to the partner by cost element. For standard rate pricing, the price to the partner may be shown as a single line calculated based on the rate.

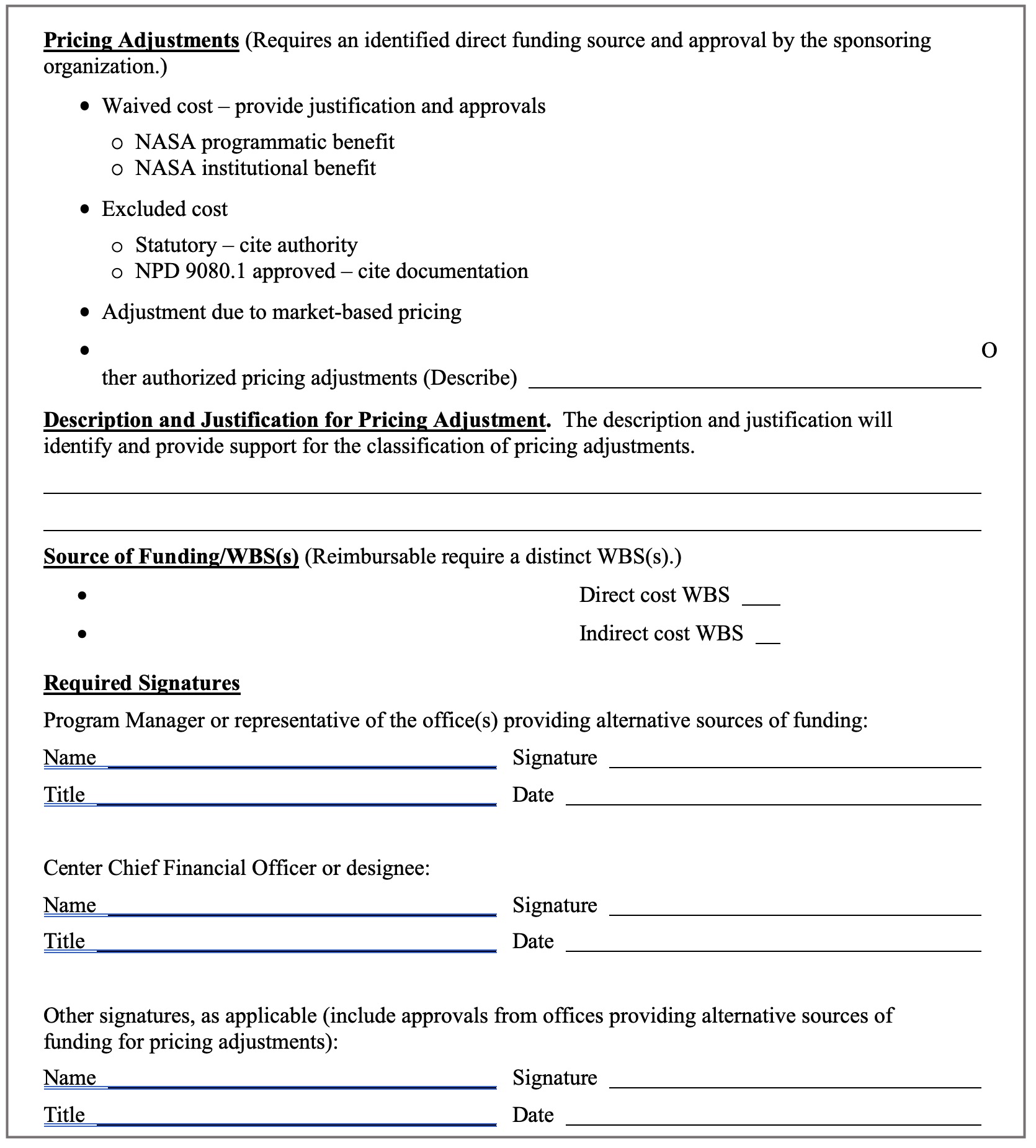

C.1.1.5 Other Information. This section contains information about the pricing adjustments and contains required signatures.

a. Type of Pricing Adjustment. Identify the appropriate pricing adjustment in accordance with section 4.3 will be associated with an appropriate signature for concurrence and approval.

b. Description and Justification for Pricing Adjustment. The description and justification should identify and provide support for the classification of pricing adjustments. For waived cost, the justification will include benefitting program/project and, as applicable, milestone impacted, how results are used, or other information useful for the determination. For excluded cost, the justification will include the authority and pricing analysis. For other authorized adjustments, the justification will include the applicable laws and regulations or market-based pricing methodology and be supportable through additional information.

c. Source of Funding. If the price to the partner is less than full cost, appropriated funds will be used to fund the difference. The direct funding source may also be used for end of agreement adjustments and will be coordinated with the direct funding source manager prior to posting. Determine whether direct or indirect costs (or both) are going to be funded with appropriated funds and, where applicable, identify the WBS(s) that will be used to fund the difference.

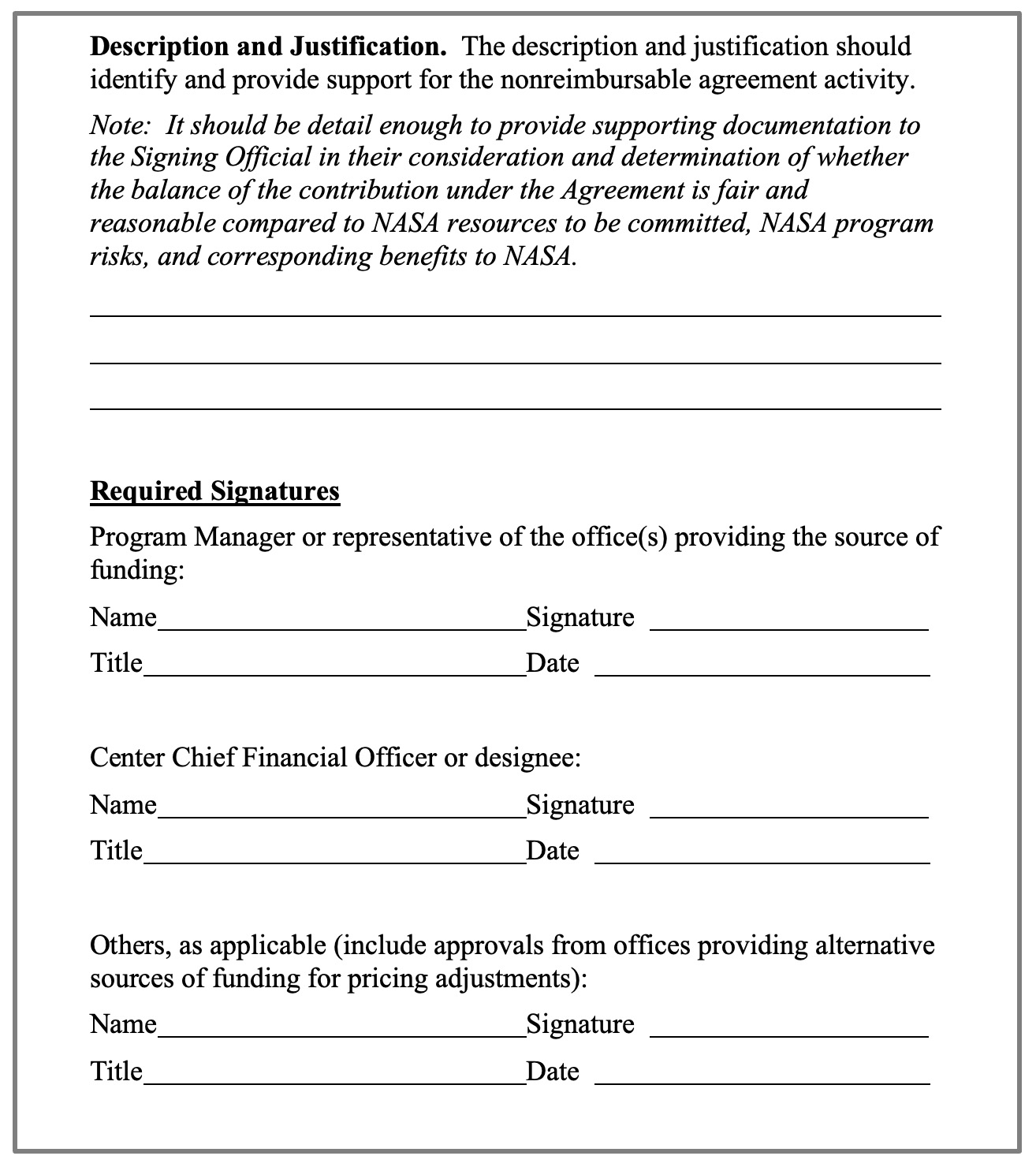

d. Signature Blocks. Names, titles, signatures, and signature dates of the Center CFO and additional approvers in accordance with this NPR and other related agreement guidance, to include Center guidance.

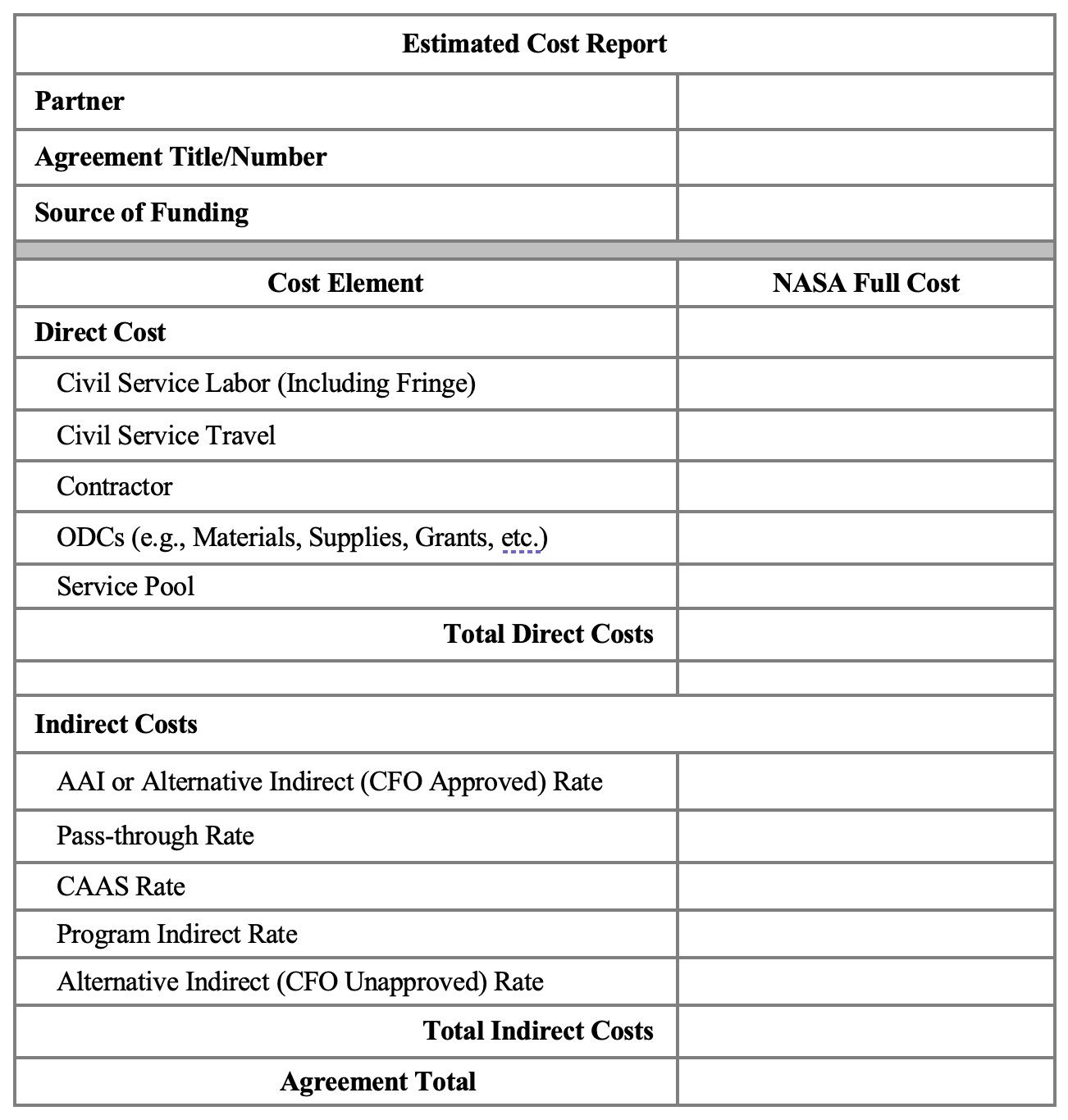

Note: The following template is representative of the minimum requirements for an ECR. Cost elements listed below include those most widely used but may not be applicable to every ECR. Additional cost elements may be included, as needed. Center CFOs may choose to use their existing EPR template in place of an ECR. However, the price to the partner should be represented as $0. Refer to section C 1.1 for instructions to applicable sections of the ECR.

| TOC | Change History | Preface | Chapter1 | Chapter2 | Chapter3 | Chapter4 | AppendixA | AppendixB | AppendixC | AppendixD | AppendixE | AppendixF | AppendixG | ALL | |

| | NODIS Library | Financial Management(9000s) | Search | |

This document does not bind the public, except as authorized by law or as incorporated into a contract. This document is uncontrolled when printed. Check the NASA Online Directives Information System (NODIS) Library to verify that this is the correct version before use: https://nodis3.gsfc.nasa.gov.