Procedural

Requirements

Effective Date: May 27, 2011

Expiration Date: November 27, 2028

|

|

NASA Procedural Requirements |

NPR 9501.2E Effective Date: May 27, 2011 Expiration Date: November 27, 2028 |

| | TOC | ChangeLog | Preface | Chapter1 | Chapter2 | Chapter3 | AppendixA | AppendixB | AppendixC | ALL | |

2.1.1 The planning process for a project or contract should include consideration of the financial management reporting requirements necessary to meet the objectives described in paragraph 1.2. Development of the proposed NF 533 reporting structure must be a collaborative effort by NASA technical, program control, procurement, financial, and resources personnel who will have a role in monitoring contractor performance, perform contract administration, or otherwise use the report data upon contract award.

2.1.2 Evidence of the collaboration shall be documented and retained by the Center Chief Financial Officer.

2.1.3 NASA's proposed reporting structure, i.e., the specific reporting categories, shall be included in the solicitation to allow prospective contractors to address their ability to meet the anticipated requirements. The final reporting structure will be determined in concert with the contractor.

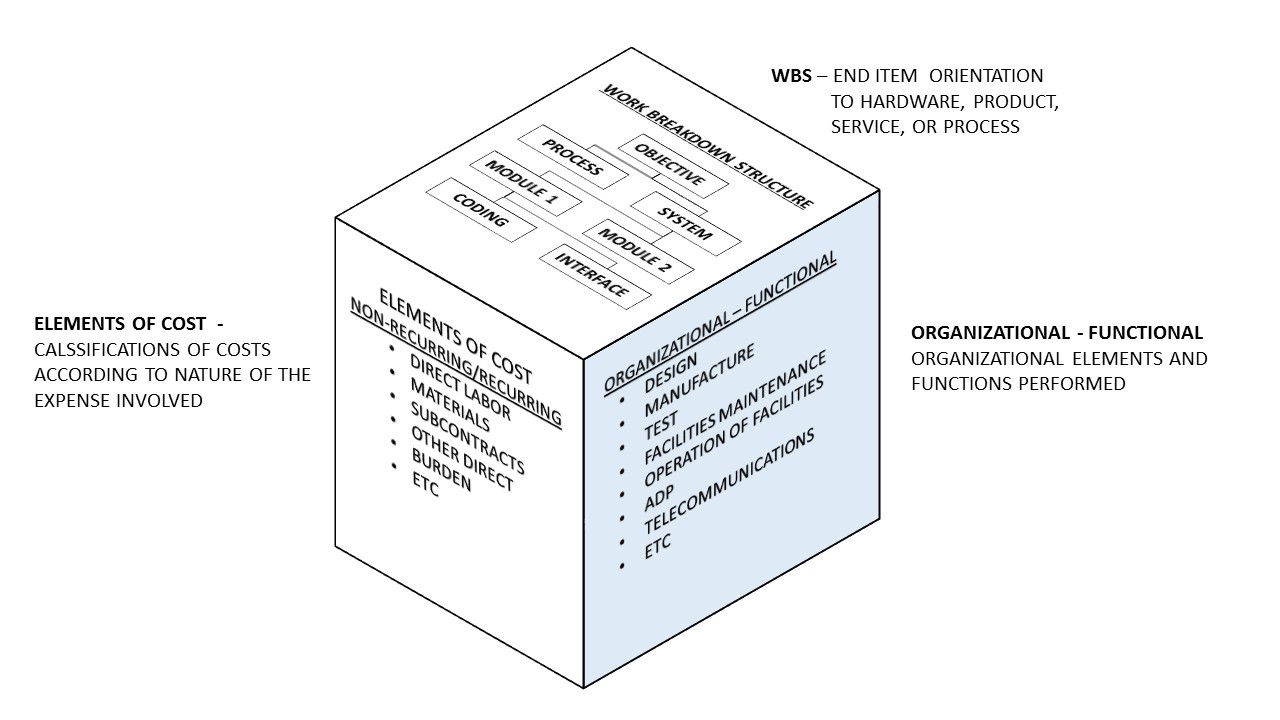

2.1.4 Both NASA and the contractor, to varying degrees, require the capability of providing an array of data from a single base, as illustrated in Figure 1, which can identify costs by organization or function, contract work breakdown structure (WBS), and type of element. The NF 533 reporting structure, therefore, shall be a matrix that provides adequate management visibility into the appropriate combination of these data.

Figure 1 Reporting Structure Data Matrix

2.2.1 The WBS is a family tree subdivision of effort required to achieve an objective (e.g., program, project, and contract). It may be hardware, product, service, or process oriented. For a contract, the WBS is developed by starting with the end objective and successively subdividing it into manageable components in terms of size, duration, and responsibility (e.g., systems, subsystems, components, tasks, subtasks, and work packages) which include all steps necessary to achieve the objective. It provides a common framework for the natural development of the overall planning and control of a contract and is the basis for dividing work into definable increments from which the statement of work can be developed and technical, schedule, cost, and labor hour reporting can be established.

2.2.2 Reference should be made to NPR 7120.5, NASA Space Flight Program and Project Management Requirements, NPR 7120.7, NASA Information Technology and Institutional Infrastructure Program and Project Management Requirements, and NPR 7120.8, NASA Research and Technology Program and Project Management Requirements, for further discussion of WBS policies and processes.

2.2.3 When NF 533 reporting will be required, the solicitation will identify the reporting categories considered necessary to meet NASA financial management information requirements. Specific contractual reporting requirements shall be tailored to reflect the way work is to be performed as set forth in the contract and to the contractors' management or reporting systems.

2.3.1 Organizational/functional data provide information on groups of activities which have a common purpose. These types of data may be required in order to:

a. Track costs by the contractors' internal organizations

b. Provide cost data for NASA functional management purposes.

c. Perform analysis-relating, organizational/functional costs to end items.

d. Relate scheduled activities to responsible contractor organizational/functional elements.

Table B Organizational/Functional Classification Examples

| Organizational/Functional Classification Examples | |

|---|---|

| 1. Engineering/Design | 7. Facilities Maintenance |

| 2. Manufacturing/Fabrication, Assembly, Test | 8. Operation of Facilities |

| 3. Reliability and Quality Assurance/ Design Review, Final Inspection | 9. Utilities |

| 10. Environmental Studies/Operations | |

| 4. Procurement/Subcontracting | 11. Transportation Services |

| 5. Mission Operations | 12. Automatic Data Processing |

| 6. Training | 13. Telecommunications Services |

2.3.2 The Center Chief Financial Officer should be consulted concerning any questions on functional classifications to be reported.

2.4.1 Elements of cost are the various uses for which resources are expended in performance of the contract. This type of information provides insight for NASA and the contractor concerning the way resources are expended and aids in comparing actual to negotiated cost rates.

2.4.2 Elements of cost are typically classified as direct or indirect (burden). It may also be necessary to determine the recurring and nonrecurring nature of cost and the performing organization and place of performance.

2.4.3 Direct costs are those which can be specifically identified with a particular objective, such as a system, subsystem, task, or function. Direct costs are typically classified as follows:

a. Labor

b. Materials

c. Subcontracts

d. Other Direct

2.4.4 Indirect costs (burden) are those which, because of their incurrence for multiple or joint objectives, are not readily identifiable to a specific objective. They are allocated to benefiting cost objectives by a statistical technique. Indirect costs are typically classified as follows:

a. Overhead

b. General and Administrative (G&A)

2.4.5 The distribution of indirect costs for reporting purposes in the same detail as direct costs are reported may be complex, especially where there are interrelated overhead pool structures. The distribution process can be simplified by restricting the distribution of overhead for reporting purposes to a logical series of group totals at a relatively high level, e.g., organization and system. Such gross treatment of burden usually does not detract from the usefulness of the reported data. It is generally desirable, however, to require a breakdown of the various types of burdens, e.g., engineering overhead, manufacturing overhead, material handling, and G&A in order to provide visibility and track actual and provisional rates.

2.5.1 The importance of selecting data elements for reporting that reflect the contractors' management philosophy and are a natural product of existing cost, budgeting, scheduling, and technical performance systems cannot be over emphasized. The contractors' internal management system shall be relied upon to the maximum extent possible, without requiring costly modifications, to furnish both detailed and summarized data for NF 533 reports. The data reported will be the basis for NASA contractor communication for financial planning and program control.

2.5.2 NASA shall ensure the contractors' management system meets the following criteria:

a. The WBS can be directly related to a specific level depicted in the technical statement of work.

b. Resource requirements and actual expenditures will be displayed on the NF 533 reports with the reporting categories directly related to the WBS on a time-phased basis.

c. Schedule line items (milestones, activities, and events), developed at lower levels of detail, can be summarized to the cost reporting level of the WBS.

2.5.3 NF 533 reports will usually require reporting by various elements of cost and subdivisions or subordinate indentures of the scope of work that are contractually designated as meaningful portions of the contract effort (WBS). When a contract includes only one subdivision of work, the reporting of elements of cost (e.g., direct labor, materials, subcontracts, other direct costs, indirect costs, G&A, and fees) will generally be sufficient. When more than one subdivision of work is included in a contract, the NASA Project Manager shall determine the level of reporting.

2.5.4 To avoid unnecessary reporting costs and ensure the appropriate level of visibility is achieved, it is important to be selective in specifying categories and levels of reporting. For example, where there is potential for high risk in a particular WBS item, more detailed visibility should be required, but it is not necessary to require the same reporting level across the WBS. Data on certain WBS items may be reported at the summary level, while others may be at the component, task, and subtask level. Careful consideration shall be given by the NASA Project Manager to the reporting requirements to ensure they are limited to items which are required and will be used in managing and monitoring the contract.

2.5.5 Reporting categories will be specified in the contract. Care will be exercised in developing reporting categories to ensure that they are consistent with the way work is to be performed on the contract and technical, schedule, and performance measurement system reports, at a management level determined adequate by NASA project management. NF 533 M and Q reports shall be structured to indicate corresponding reporting categories and levels of detail. Not all the reporting categories discussed herein are required on all contracts, nor are all categories which may be required discussed.

2.5.6 Where the contract effort is divided into separate "schedules" for each fiscal year or other period or provides for the exercise of options to continue the contract, reporting should be structured in the manner most appropriate to the contract provisions. Each report shall, however, contain a summary of total contract cost, which may be broken out by the various cost elements, indicating cumulative actual costs for all "schedules" or exercised options from inception of the contract to date.

2.5.7 In addition to the summary, the contractor shall report cost at a detailed level by elements of the contract WBS.

2.5.8 Totals on the summary report provided by the contractor shall match totals derived from all contract WBS elements. If the portion of the reports structured by WBS does not indicate each individual cost element as reported in the summary pages of the report, values reported for the various WBS items will still reflect all cost elements, so that the total cost of all WBS items agrees with the total by elements of cost (total cost at the contract summary level).

2.5.9 For service contracts, the NF 533 reports shall be structured to provide cost data in the program/functional management classifications by which NASA managers relate in-house activity. Further detail may be required for items such as tasks, work orders, or other significant and identifiable phases of work or services being procured. Such detail may be supported by information on direct labor hours, direct labor costs, and other cost elements appropriate for monitoring the subdivisions of work.

2.5.10 NF 533 reporting structures shall be designed to facilitate accounting for costs in accordance with NASA's financial coding structure and to provide as direct linkage as practicable from the work performed by the contractor to the NASA appropriation funding that work. This is the level prescribed by NASA management to maintain control and account for costs and subsequent disbursements in accordance with Congressional appropriations.

2.5.11 To ensure all capitalized Property, Plant, and Equipment (PP&E) is identified and assigned a unique NASA WBS element, contractors shall obtain approval prior to purchasing or beginning fabrication of any PP&E with an anticipated total acquisition cost of $500,000 or greater not specifically identified in the contract, in accordance with 48 CFR 1852.245-70, Contractor Requests for Government-Owned Equipment.

2.5.12 For all PP&E purchases and fabrications (specifically identified in the contract or otherwise approved) identified by NASA as capitalized items, the NF 533 reporting structure shall provide for the accumulation and reporting of cost for each individual item in separate reporting categories.

2.5.13 Research and development contracts with cost-sharing provisions require NF 533 reporting, which provides summary data for total contract actual and projected costs, with a further breakdown indicating the NASA-funded portion of those costs.

| TOC | ChangeLog | Preface | Chapter1 | Chapter2 | Chapter3 | AppendixA | AppendixB | AppendixC | ALL | |

| | NODIS Library | Financial Management(9000s) | Search | |

This document does not bind the public, except as authorized by law or as incorporated into a contract. This document is uncontrolled when printed. Check the NASA Online Directives Information System (NODIS) Library to verify that this is the correct version before use: https://nodis3.gsfc.nasa.gov.